Long combo is a bullish option strategy with two legs. It is similar to synthetic long stock, only with a gap between strikes. It has unlimited potential profit and limited loss (although the loss can also be very large if underlying falls a lot).

Setup

Long combo is set up just like synthetic long stock, using a long call and short put option. Only difference from synthetic stock is that the call strike is higher than the put strike.

To create a long combo position:

- Buy a call option.

- Sell a put option with lower strike and same expiration date.

Strike Selection

The strikes are typically selected in such way that both the options are out of the money when the position is opened, which means the call strike is above current underlying price, while the put strike is below.

However, this is not a universal rule. The position is still a long combo even when both strikes are above or both are below the underlying price. Only hard requirement is that the call strike is higher than the put strike.

Some sources use the name long combo for any position that includes long call and short put option, regardless of strikes. Synthetic long stock, where both strikes are the same, would also be considered long combo in this wider meaning.

Example

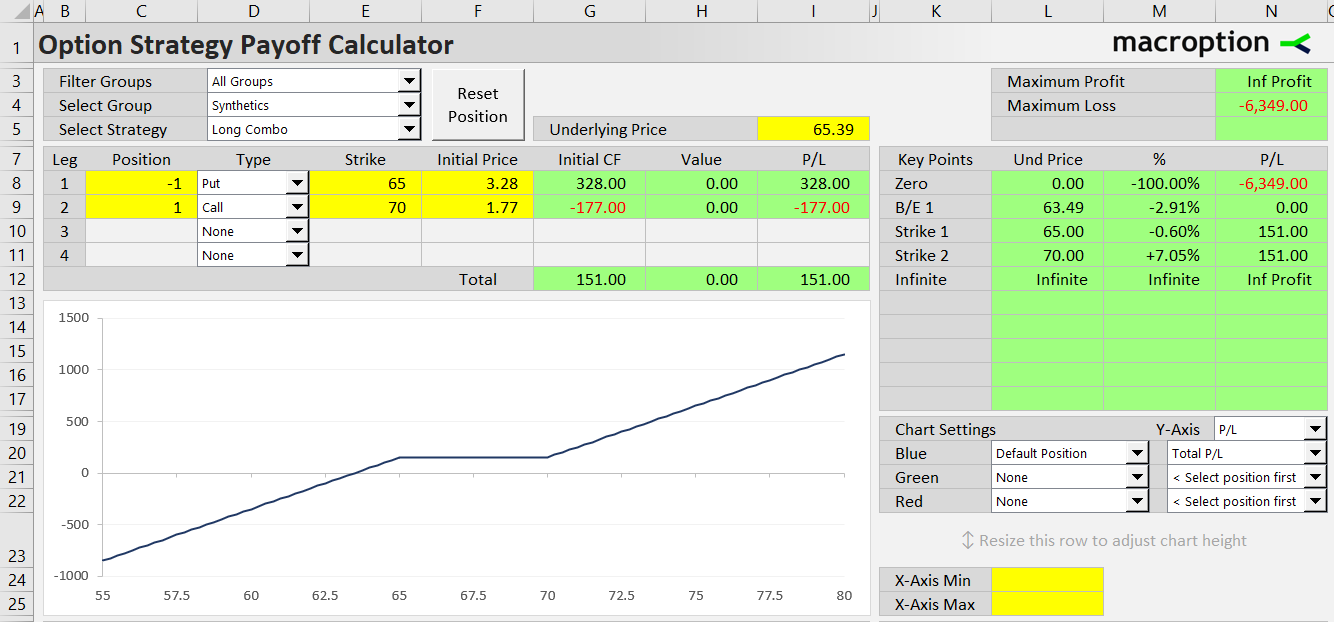

For example, consider a stock currently trading at $65.39 per share (this is the underlying price). We can create a long combo position with the following option trades:

- Buy the 70 strike call option for $1.77 per share.

- Sell the 65 strike put option with same expiration for $3.28 per share.

Cash Flow

Initial cash flow when setting up a long combo position can be positive or negative, depending on relative prices of the options. If the call option is more expensive than the put option, initial cash flow is negative, because we are buying the call and selling the put. Conversely, when the put option premium is higher (as in the example above), initial cash flow is net positive.

Long combo initial cash flow = put premium received - call premium paid

In our example, initial cash flow is $3.28 per share received for the put option minus $1.77 paid for the call, which is net credit of $1.51, or $151 for one option contract (assuming option contract size of 100 shares).

Payoff at Expiration

The effect of underlying price on payoff at expiration is very simple: the higher the underlying, the greater the profit (or smaller the loss).

Payoff Diagram

Although profit or loss generally increases with underlying price and the payoff diagram resembles long underlying position (or synthetic long stock option strategy), it is not a constantly upward sloping line. There is a gap between the put and call strike, where P/L does not increase.

This is because both the options are out of the money and expire worthless. Total profit or loss from the trade is constant and equals initial cash flow.

Maximum Profit

Above the call strike, the position behaves like a long call option. Profit grows to theoretically infinite.

Maximum Loss

Below the put strike, the payoff is like a short put option. Total loss increases with falling underlying price.

Maximum loss occurs when the underlying falls to zero.

**Long combo max loss = put strike - initial cash flow

= put strike + call premium paid - put premium received**

In our example, maximum loss is 65 + 1.77 - 3.28 = $63.49 per share or $6,349 for one contract.

Break-Even Point

Depending on initial cash flow, the break-even point can be either above the call strike or below the put strike. It is never between the strikes, because P/L is constant in that area.

If the call option is more expensive than the put option when opening the position, initial cash flow is negative (and so is the loss between the strikes). The break-even point is above the call strike and equals:

Long combo B/E = call strike - initial cash flow

Note that initial cash flow is negative in this case, so the break-even point is above the call strike. We can also write the formula as:

Long combo B/E = call strike + net initial cost

If the put option is more expensive, initial cash flow is positive, and the break-even point is below the put strike:

Long combo B/E = put strike - initial cash flow

Our example is the second case (put more expensive than call) and the break-even price is:

65 - 1.51 = 63.49

Note that the break-even price equals maximum loss in this case. This makes sense, as total loss increases dollar-for-dollar below the break-even, all the way to zero underlying price. However, it only holds when the break-even is below the put strike (in the other case, when the break-even is above the call strike, it equals maximum loss + distance between call and put strike).

Related Strategies

- Short combo - the inverse position (long put + short call with higher strike)

- Synthetic long stock - similar to long combo, but with the call and put strikes equal