Iron condor is a non-directional option strategy with four legs. It has limited loss and limited profit.

Setup

An iron condor is set up at four different strikes, in this order from lowest to highest:

- Long put option (lowest strike).

- Short put option.

- Short call option.

- Long call option (highest strike).

The order of strikes matters. The put strikes are lower than the call strikes. The short options are at the inner strikes, while the long options are at the outer strikes.

The strikes are typically chosen in such was that the current underlying price (when opening the position) is approximately halfway between the two inner strikes.

The distance between the two call strikes (long call and short call) must be the same as the distance between the two put strikes (long put and short put). This distance is called the wing width, as the outer strike long options are called wings of the condor, while the inner strike short options are the body.

The distance between the two short options (the inner strikes) can be different than the wing width. But the two wings must have the same strike distances, which ensures that the position is symmetric and has no directional bias (a modified version of iron condor with unequal wing widths and directional bias is called broken wing iron condor).

All options must have the same expiration date. All legs must have the same number of option contracts (long or short).

Example

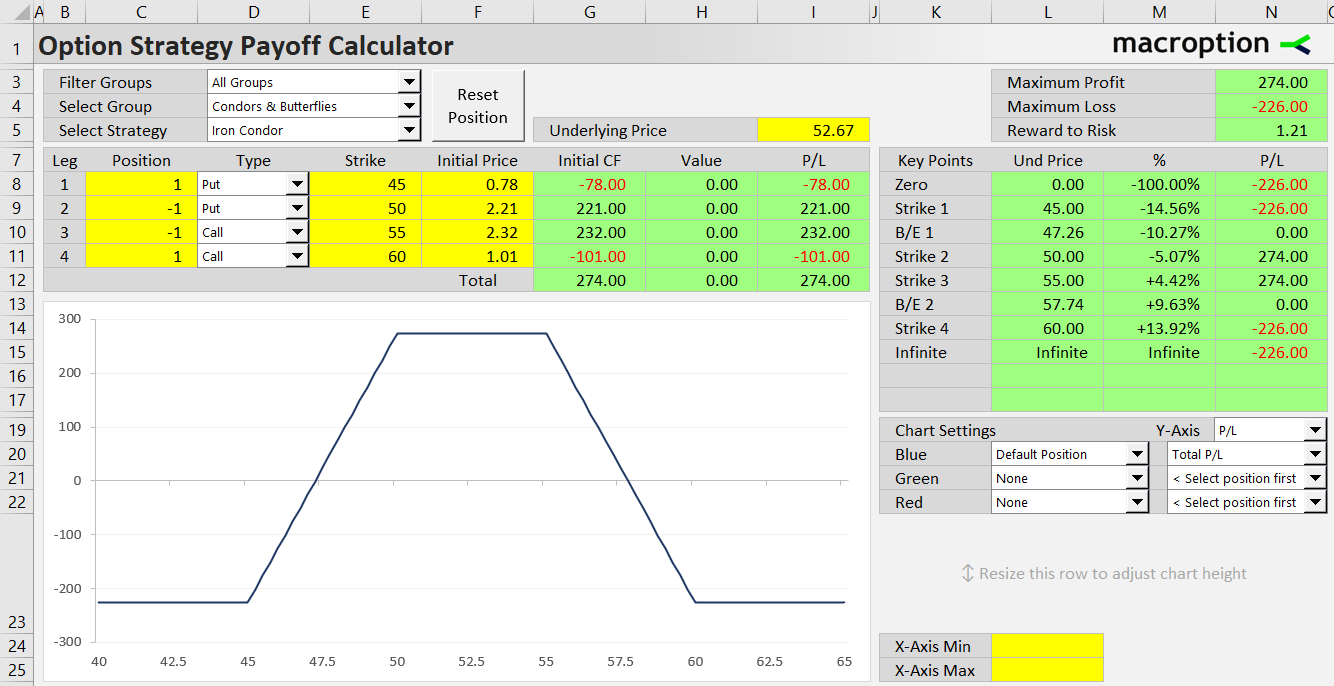

Let's say underlying stock is trading at 52.67. We can open an iron condor by making these transactions:

- Buy 45 strike put for 0.78 per share ($78 for one option contract).

- Sell 50 strike put for 2.21 ($221).

- Sell 55 strike call for 2.32 ($232).

- Buy 60 strike call for 1.01 ($101).

Underlying price 52.67 is approximately halfway between the inner strikes (50, 55) and wing width is the same for both the puts (50-45) and the calls (60-65), which ensures symmetry of our position's risk profile.

Cash Flow

Initial cash flow from opening an iron condor position is positive - it is a credit strategy. The reason is that the options we are selling (the inner strikes) are more valuable than those we are buying (the outer strikes).

Net premium received is what we gain from selling the short call and short put, minus what we pay for buying the long call and long put. In our example it is 2.74 per share (2.32 + 2.21 - 1.01 - 0.78), or $274 for one contract.

Payoff at Expiration

The objective of an iron condor trade is for underlying price to stay between the inner strikes and all the four options to expire worthless.

Payoff Diagram

The payoff diagram shows maximum profit between the two inner strikes. When underlying price gets above the short call strike or below the short put strike, total profit decreases and as some point between the short and long strike it turns to loss. On both sides, the loss stops growing at the outer strike, where the respective long option start to hedge further losses from the short option.

Maximum Loss

Maximum loss from iron condor occurs when underlying price ends up at or above the long call strike or at or below the long put strike. The difference between the short and long strikes (the wing width) is the most we can lose at expiration - it is the amount by which the intrinsic value of the short option is greater than the intrinsic value of the long option if the latter is in the money.

Iron condor maximum loss = wing width - net premium received

Maximum Profit

Maximum profit is reached between the inner strikes, where all options expire out of the money and we keep the entire premium received when opening the position.

Iron condor maximum profit = net premium received

Risk-Reward Ratio

The risk-reward ratio improves when wing width becomes smaller (this reduces both maximum profit and maximum loss).

Break-Even Points

Iron condor has two break-even points - one between the put strikes and another between the call strikes. The distance of the break-even price from the respective short strike price equals net premium received (and the distance from the long strike equals the maximum loss).

Iron condor B/E #1 = short put strike - net premium received

Iron condor B/E #2 = short call strike + net premium received

Greeks

Delta

When opened with current underlying price halfway between the inner strikes, iron condor is delta neutral.

Delta changes as underlying price moves to one or the other side (this is measured by gamma).

Gamma

Iron condor has negative gamma. This means that delta increases when underlying price falls, and decreases when underlying price grows.

That said, gamma turns positive as underlying price approaches one of the outer long strikes, where the hedge takes its effect.

Theta

Theta is positive. Other things being constant (underlying price staying between the middle strikes), the position profits from passing time.

Vega

Vega is negative - the position loses when implied volatility increases. Again, this changes when underlying price gets further away from the inner strikes.

Related Strategies

- Reverse iron condor - the inverse position, which is long the inner strikes and short the outer strikes

- Iron butterfly - the short call and short put strike is the same

- Long call condor - all legs are calls

- Long put condor - all legs are puts

- Short strangle - unhedged alternative to iron condor (without the long options) - greater potential profit, but also unlimited risk