Collar is a bullish option strategy with three legs, including long position in the underlying asset. It has limited loss and limited profit.

Setup

Collar is one of very few option strategies which involve all the three types of instruments: the underlying asset, a call option, and a put option. It combines the features of two other popular strategies with underlying: it has a short call like the covered call strategy and a long put like the protective put strategy.

To create a collar position:

- Buy (or already own) the underlying asset.

- Buy a put option (for downside protection).

- Sell a call option (to help pay for the put and possibly earn extra income).

Main Rules to Remember

The call and put options should have the same expiration date. Similar positions can be created where the options have different expirations, but then it is not the collar strategy as commonly understood, and the payoff profile described below does not apply (and the position may be exposed to extra risks).

The call option's strike price should be higher than the put strike.

The position sizes should match. There should be same number of contracts for the short call and long put, and the number of shares or units of the underlying should also match (taking the option contract multiplier into consideration, e.g. 100 shares for one option contract for US traded stock options).

Example

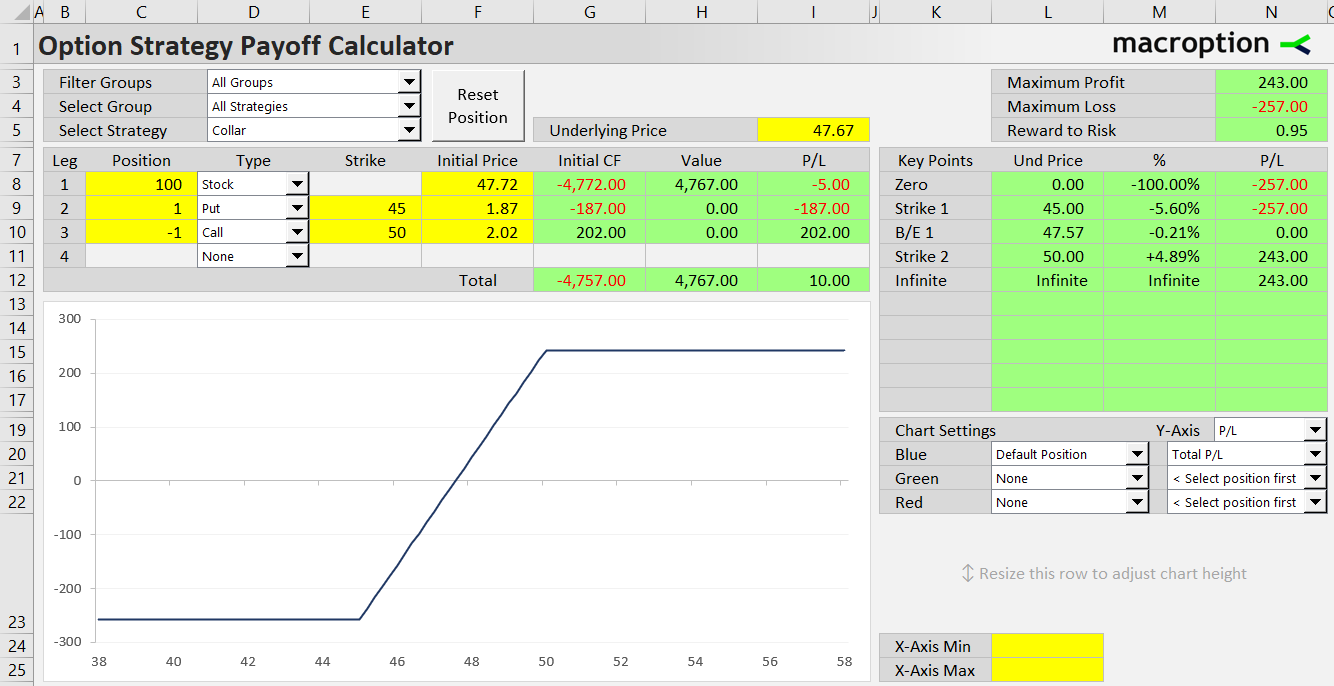

Let's say we buy 100 shares of a stock for $47.72 per share. To create an option collar on this position we need to make the following trades:

- Buy one contract of the 45 strike put option for $1.87 per share.

- Sell one contract of the 50 strike call option with same expiration for $2.02 per share.

Cash Flow

When we consider the initial purchase of the underlying stock being part of the collar position, total initial cost is obviously very high, as we need to pay for the shares.

Looking only at the option legs, their initial cash flow can be either a credit (lowering our cost of the stock position) or debit (adding to the cost). This depends on relative prices of the call and the put.

Collar initial cost = initial stock price + put premium - call premium

In our particular example, we paid $4,772 for the 100 shares and $187 for one put option contract. We have received $202 for the short call contract. In this case, the call price was higher than the put price, so the options improved total initial cost, although only very little (by $15, or $0.15 per share). Total initial cost of this position was $4,757, or $47.57 per share.

Payoff at Expiration

Assuming the call and the put have same expiration date, total profit or loss at expiration is a function of underlying price.

Payoff Diagram

Payoff diagram of the collar strategy looks similar to bullish vertical spreads (bull call spread and bull put spread). It has limited constant loss below the lower (put strike), increasing P/L between the strikes (dollar for dollar with underlying price), and constant profit above the higher (call) strike.

For detailed explanation and examples of what happens under different scenarios (maximum loss, maximum profit, in between) and how the individual legs contribute to total P/L in each case, see collar payoff.

Maximum Profit

Maximum profit applies at or above the higher (call) strike. It is calculated as:

Collar max profit = call strike - initial cost

In our example:

50 - 47.57 = $2.43 per share = $243 for one contract

Maximum Loss

Maximum loss applies at or below the lower (put) strike. Its formula is:

Collar max loss = initial cost - put strike

In our example:

47.57 - 45 = $2.57 per share = $257 for one contract

Risk-Reward Ratio

When collar is opened with underlying price about halfway between the two strikes, as in out example, the sizes of maximum profit and maximum loss are quite similar and risk-reward ratio is close to 1:1. It may be a bit better or worse, depending on the exact initial cost relative to the strikes.

Break-Even Point

There is one break-even point, located between the strikes. Its calculation is actually very simple: it equals initial cost.

Collar B/E = initial cost

Collar B/E = initial stock price paid + put premium paid - call premium received

Strike Selection

The relative distance of call and put strikes from underlying price determined the position's initial cost, as well as risk profile.

Choosing a higher call option strike increases net initial cost, because the call is further out of the money and therefore call premium received is smaller. At the same time it extends the window where gains in underlying price translate to profit (because that is capped at the call strike).

Choosing a lower put strike reduces initial cost, because the put is further out of the money and therefore can be purchased cheaper. At the same time, with lower put strike, the downside protection kicks in later if the underlying goes down.

Related Strategies

- Bull call spread - vertical spread with similar payoff (without the underlying position)

- Bull put spread - another vertical spread with similar payoff, this time with puts

- Covered call - similar to collar, but without the downside protection

- Protective put - underlying with a put option, without the short call